December is the month for lots of celebrations as we hosted a few rounds of gatherings with family and friends. The kids had lots of fun and it was generally a chill period, as everyone basked in the holiday season.

I was reading “The life-changing manga of tidying up” by Marie Kondo and was reminded the benefits of having a organized home with lesser stuff. I think the main benefit of have a neat place is not just the practical sense of it but more of the mental calmness that it brought into our lives. Our homes are meant for us to rest our mind and body and not for us to spend so much time to upkeep. Tidying-up or decluttering becomes an easier process once you have less stuff in your home and you do it regularly.

Looking forward to the latest Marie Kondo’s Netflix series which will debut in Jan 2019.

On that particular day, I was tasked to take care of a 7 year old boy together and his mother, who is his primary caretaker. He required a wheelchair throughout the whole outing. On numerous occasions, I had to help him to board and alight the bus as his mother was struggling to carry him. At the end of the day, the boy and the mum sincerely thanked me for organizing the trip and they really enjoyed it. I spoke with the staff after the trip to understand more about his condition and was shocked by her reply. She listed four different kind of conditions – cerebral palsy, global development delay, ex premature and spastic hemiplegia. I had to google the meaning of each condition to understand it better and basically it was something that requires lifelong care. It was a rather daunting moment for myself and it really made me ponder a lot.

I can never imagine what his parents will have to go through on a daily basis. As a father of two young kids, I could not help but feel how fortunate we really are. This makes our down days pale in comparison with what the boy or his mother might be coping on a daily basis. It also reinforced the conviction that we should live life with more gratitude than ever.

Fitness Update

As I broke my ACL more than a month ago during a soccer match, I have been religiously following the fitness regime as recommended by my physiotherapist. I was able to get back to slow jogging and was also able to practise yoga with much relief. The physiotherapist also taught me how to run in a proper manner so that I could prevent future injuries and strengthen the overall fitness of my body. This episode allowed me to appreciate the effectiveness of physiotherapy and the working mechanics of our body. I had initially thought that it would be hard for me to go back to extreme sports but apparently, that might still be in the cards for me. I have been progressing well with my physio sessions and hopefully my upcoming appointment in February with the orthopedic surgeon will provide some bearing as to if a surgery is still required for my condition.

My weekly fitness routine – Post ACL tear

(To strengthen my glutes, quadriceps, hamstrings and calves):

1) Daily static exercise routine (4 sets of each exercise for both legs):

1. 12 x Front supported single leg squat

2. 12 x Tip-toe front supported leg squat

3. 12 x Split squat

4. 12 x Standing single leg raise

2)2 x Staircase climbing 30 levels up and down plus static exercise on both ground and top level. (Done during lunch time in my office building)

3) 2 x 3 km slow jogging (average 6 – 7 mins / km pace)

4) 2 x Yoga Lesson

5) Using the Great Eastern Get Great app and enrolling in the National Steps Challenge , I’m currently trying to average 10,000 steps daily and redeem vouchers.

Family

Below are some of the simple activities we do on weekends:

Financial Update

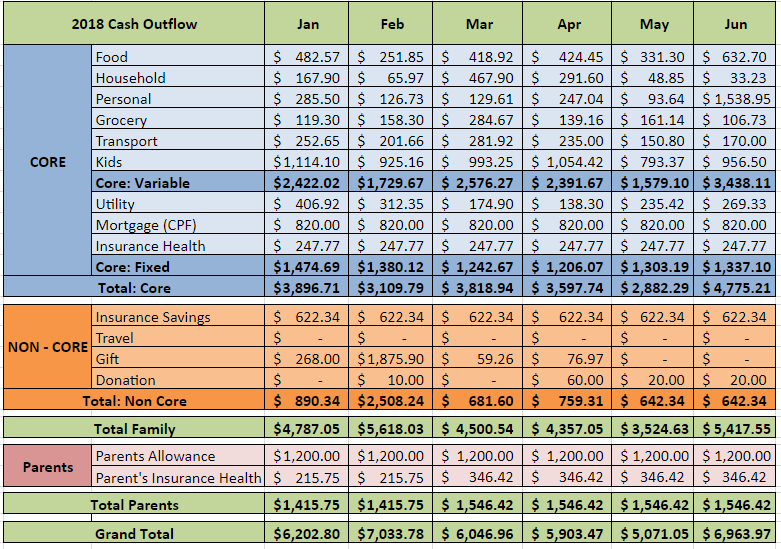

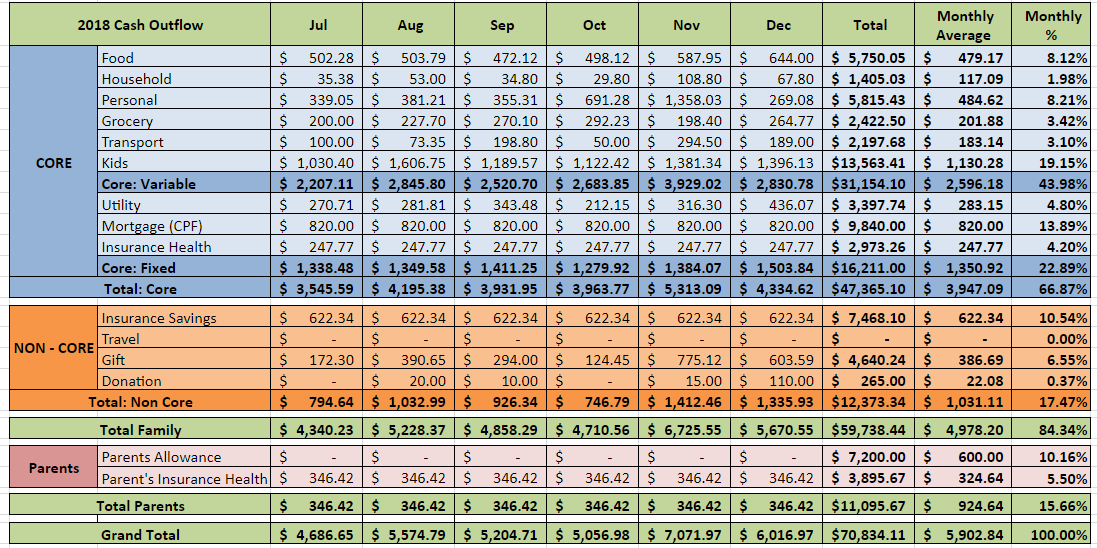

We had managed to compile our December cash outflow and below is a snapshot:

FAMILY ($5,670.55)

Core: Variable ($2,830.78)

Food ($644.00)

$644.00 – Meals for our family of four (this includes snacks and drinks, etc.)

Household ($67.80)

$27.90 – Newspaper subscription for Kate’s parents

$39.90 – Bedsheets

Personal ($269.08)

$36.00 – Haircut (whole family of 4)

$120.00 – Yoga lesson (Dave and Kate)

$59.80 – Dave’s Clothes

$38.70 – Kate’s Skincare and Toiletries

$12.00 – Kate’s Vitamins

$2.58 – iCloud 50 GB storage (monthly fees for Dave and Kate)

Groceries ($264.77)

$264.77 – Mainly groceries and some other household items from the supermarket

Transport ($189.00)

$189.00 – Ezlink card reload for both of us (for bus and train rides)

Kids ($1,396.13)

Ally

$850.00 – Full day child care for Ally (inclusive of some optional enrichment class)

$290.00 – Chinese enrichment Term 1 2019 course fees (8 sessions)

$30.00 – Year end performance tickets

$90.00 – Family Trip to SEA Aquarium

$13.68 – Activity books

$28.90 – Traditional Chinese Medicine (TCM)

$23.70 – Clothes

$30.00 – Timezone (Arcade)

Ashton

$20.00 – Kids Amaze (indoor playground)

$12.00 – Train rides

$7.85- Diapers / misc

Core: Fixed ($1,503.84)

Utility ($436.07)

$129.73 – Electrical/Water/Gas

$78.00 – Property Services and Conservancy Charges

$228.34 – Mobile / Internet

Mortgage ($820.00) – Paying using our CPF. 20 year bank loan (First 3 years fixed interest and floating on the 4th year onward pegged against the FHR9 rate). We would like to maintain an arbitrage on this home loan as the interest is less than 2% and we might repay it in full should the interest spike up when we reach FI.

Insurance – Health ($247.77) – Insurance premiums – hospitalization and outpatient (annual premiums amortized into 12 months)

Non-Core ($1,335.93)

Gifts ($603.59)

$215.96- Christmas meals with family and friends

$387.63 – Christmas gifts for family and friends

Donations ($110.00)

$110.00 – Charity gifts and donations

Insurance – Savings ($622.34) – Insurance premiums – includes savings and whole life policies (annual premiums amortized into 12 months)

PARENTS ($346.42)

Insurance – Health ($346.42) – Insurance premiums – hospitalization and outpatient (annual premiums amortized into 12 months)

Target FI family cash outflow (excluding parents and mortgage) = $5,000 per month (core $3,500 and non-core $1,500)

Legend:

Family:

Core is the variable / fixed cash outflow incurred for the month as “operational expenses”. This is the minimum to run our household comfortably and is the amount we will still be incurring even when we are not working.

Of course, we could further reduce this with our minimalist lifestyle by cutting back on childcare ($850) and fully pay off our mortgage ($820). This will potentially reduce our family Core cash outflow by 40% whereby we could operate our family within a budget of $2,500.

Non-core is the category that includes travelling, donations/gifts, savings insurance and things that will enhance our happiness level, security and sense of purpose over the long run. Our savings insurance policies here to show that these are additional savings we have and we might monetize this when our kids gets older. We think that these are important elements to move higher up on the pyramid under the Maslow’s hierarchy of needs. We want to maintain this as long as possible to have something to look forward in future.

Parents:

We would like to continue paying for their health insurance as long as both of us are still gainfully employed.

Summary for December

Family ($5,670.55):

Core ($4,334.62)

This month our family core cash outflow is the slightly above average mainly due to Ally’s Chinese enrichment class which will start next year.

Non-core ($1,335.93) :

This category is also above average due to Christmas gifts and celebration during this festive season. We also made some donations to charities.

Parents ($346.42):

We finally reduce our parents allowances significantly by topping up with an initial lump sum into their retirement account (CPF Life) which will guarantee payment to them for a lifetime. This will transfer the reliance on us to give them cash allowances to CPF Life which works like an annuity. So we are now only paying for their health insurance which should slowly creep up as they age.

Grand Total ($6,016.97)

We spend about $6 k based on the overall cash outflow this month and it is close to our average for this whole year.

Will do a full year analysis for 2018 soon. Stay tune!

Hi, I’m a reader from the US. I’m interested in the fact that you support your parents. My husband is Asian (Taiwanese by way of Brazil) and I’m white. He and I have differing norms regarding supporting family. I’m white and grew up with only the idea of supporting your children. Financial advice here is to support yourself first, then your children. It doesn’t mention parents. I’m overwhelmed by the idea of supporting elders in addition to our son when we make OK, but not great salaries, and have little safety net within our national system. I feel like such a bad person but this seriously is difficult for me to consider, especially when his parents have little yet travel more than we do. There’s more to it than that, but I’m interested in cultural differences when it comes to finances and what your thoughts are?

I would think its very different here in Singapore as our grandparents were mostly immigrants. So they started out really poor and the second generation and third generation ( thats us) make better income as compared to 50 years ago. The first generation spend most of their resources to raise the second generation and so on. Its trickles down like a domino effect but the responsibility towards giving parent allowance will slowly dissipate as we become wealthier. Like for us, we do not really expect our kids to support us during retirement as we have our own retirement plans. Even our parents already have some form of retirement plans but we just supplement it as a token for raising us. I don’t think it’s a compulsory thing and its really about how comfortable you are when you do that. Think that might be the difference between Western and Asian culture. We as the younger generation generally thinks that retirement should be your own responsibility.