(Originally shaped over two decades of investing)

This year, I’ll be revisiting how some of my thinking has changed over time—including how I approach money and investing. This is the start of a series that explores not just what I invest in, but how I think about risk, reward, volatility, and building wealth with a solid foundation.

The Beginning: An All-Stocks Portfolio

I started investing in stocks in 2004.

At the time, it felt natural. I was young, had stable income, and believed time was my greatest advantage. The market, despite its volatility, seemed to reward those who stayed patient. Market swings were something I read about in the news, not something that kept me up at night.

So I built an all-stocks portfolio focused entirely on growth.

Looking back, it wasn’t wrong. It was appropriate for that season of my life.

What an All-Equity Portfolio Taught Me

An all-stocks portfolio builds conviction in ways nothing else can.

You learn to sit through market noise. You learn that markets fall and eventually recover. You learn that time has a way of smoothing things out.

Most importantly, you learn to stay invested even when it’s uncomfortable.

These lessons shaped how I think about investing even today. Without that early exposure to volatility, I doubt I would have developed the patience required for long-term wealth building. The experience taught me that investing is as much a psychological discipline as it is a financial one.

But over time, I realized that patience alone isn’t the same as resilience.

When Growth Stopped Being My Only Goal

Life became less straightforward as the years passed.

Responsibilities increased as a parent. Time felt more precious. Decisions carried consequences that affected more than just myself.

My portfolio grew, but so did the mental weight attached to it. Market swings that once felt abstract started interfering with my sleep, my focus, and my mood. A 20% drawdown in my twenties was a statistic. In my forties, with a family depending on that portfolio, it became personal.

The issue wasn’t volatility itself—it was concentration risk.

Too much of my financial future depended on a single assumption: that growth would continue indefinitely, that markets would always bounce back quickly, that I would remain emotionally detached during major drawdowns.

That assumption went largely unchallenged in my twenties. It didn’t survive my forties.

The Gradual Shift Toward Balance

The evolution was gradual rather than sudden.

I didn’t wake up one day and sell all my stocks. I still believe equities are among the most powerful long-term wealth-building tools available. The key word being “among”—not “only.”

But I started diversifying beyond just stocks:

- Income-focused investments and dividend ETFs

- Global market exposure via broad-based ETFs

- Bonds for stability and ballast

- Cash buffers for emergencies and dry powder for opportunities

- Real estate investments

- Alternative assets including gold and Bitcoin

None of these additions were about chasing higher returns. They were about reshaping how risk showed up in my life.

Returns matter, but the journey to those returns matters more than spreadsheets typically account for. A portfolio that delivers 8% annually with manageable volatility beats one that delivers 12% but causes sleepless nights and panic selling during downturns.

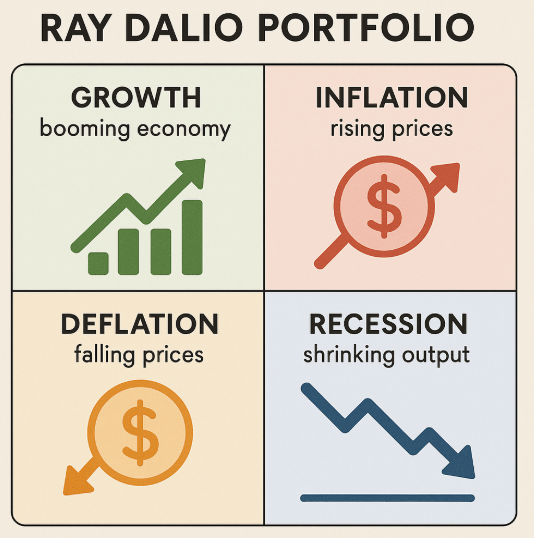

A Framework That Changed My Perspective

My thinking crystallized when I first encountered Ray Dalio’s All Weather Portfolio many years back.

What struck me wasn’t the specific asset allocation—it was the fundamental question it asked:

What kind of portfolio can weather different economic environments?

Growth. Inflation. Deflation. Recession. Expansion.

Instead of trying to predict which environment would come next, the All Weather approach accepted uncertainty as a permanent condition of investing. This was profound. It shifted my mindset from “what will happen?” to “what might happen and how prepared am I?”

That insight stayed with me.

Reading Ray Dalio’s “Principles” and later “The Changing World Order” and of course the 1929 Great Depression added another dimension. Markets aren’t just driven by corporate earnings and innovation—they’re shaped by long cycles of debt, geopolitics, currency systems, and human behavior. These forces operate on timescales far beyond quarterly earnings reports.

Volatility stopped looking like a problem to solve. It started looking like a feature to prepare for.

Minimalism, Applied to Investing

Minimalism was never really about owning fewer things.

It was about removing single points of failure from your life and creating optionality.

That principle translated naturally into how I think about money. Just as we simplified our physical space to reduce maintenance and mental clutter, I began applying the same logic to my portfolio. The goal wasn’t complexity for its own sake, but resilience through thoughtful simplification.

A minimalist portfolio, to me, isn’t a narrow one focused on a few concentrated holdings. It’s one that doesn’t depend on a single narrative being true—whether that’s perpetual growth, stable inflation, or rational markets.

Diversification isn’t about mathematical optimization or chasing the efficient frontier. It’s about intellectual humility. It’s acknowledging that I don’t know which regime comes next, so I’ll prepare for multiple outcomes.

What I Prioritize Today

Today, I don’t optimize for maximum returns.

I optimize for:

Long-term sustainability – A portfolio that can compound for decades without requiring constant intervention or rebalancing.

Emotional resilience during downturns – The ability to stay invested when others panic, not because I’m brave, but because my portfolio is designed to weather storms.

Risk management across different economic regimes – Protection against scenarios I can imagine and humility about scenarios I can’t.

The ability to stay invested without constant reassurance – I check my portfolio occasionally, not obsessively. It should work quietly in the background.

Most of all, I optimize for peace of mind.

A portfolio that demands constant monitoring, explanation, or conviction maintenance is too fragile for the life I want to live. Financial independence isn’t just about the number in your account—it’s about the psychological freedom that comes with knowing you’re prepared for uncertainty.

Investing as Financial Infrastructure, Not Accumulation

Investing used to feel like a way to accumulate wealth.

Now it feels more like building infrastructure with a strong foundation.

Strong financial infrastructure allows your attention to move elsewhere—toward meaningful work, family, personal growth, and experiences that matter. It’s not that money becomes unimportant; it’s that a well-built portfolio fades into the background, supporting your life without demanding constant attention.

This shift mirrors how we think about our home. We don’t constantly rearrange furniture or question whether the foundation is solid. We built it thoughtfully once, maintain it periodically, and let it serve its purpose while we focus on living.

Financial independence, for me, was never about escaping work or responsibilities.

It was about creating stability that provides optionality in life—the freedom to make decisions based on values rather than societal pressure. The freedom to take meaningful risks in work because your downside is protected. The freedom to spend time with family without anxiety about missing career opportunities.

And that fundamental shift in purpose changed everything about how I invest.

Looking Ahead

This approach continues to evolve. As I gain more experience—and as markets, economies, and my personal circumstances change—I expect my thinking will continue to adapt.

But the core principle remains:

Investing should support the life you want to live, not become the life you live.

In the next part of this series, I’ll discuss why I shifted to a multi-asset approach, focus on asset allocation to build portfolio resilience.

This is a personal reflection on how I think about investing over time. It’s shaped by my own circumstances and priorities, and isn’t intended as financial advice. Everyone’s situation is unique, and what works for me may not work for you. Consider consulting with a qualified financial advisor for personalized guidance.

2 thoughts on “Investing Lessons Part 1: How My Investment Philosophy Evolved over more than two decades”

Comments are closed.