After sharing how my investment approach evolved over two decades in Part 1, the natural question becomes: how does it all fit together?

Asset allocation sounds technical, but at its core, it’s simply deciding how to distribute resources across different asset classes—and more importantly, why.

From Theory to Reality: Our Great Resignation Test

The true test of any allocation strategy isn’t how it looks on paper. It’s whether it works when life forces difficult decisions.

In 2022, Kate and I executed our “Great Resignation”—a complete mid-career pivot to a different industry that would have been impossible without years of deliberate portfolio construction. I wrote about this previously here.

When I was made redundant during COVID, we faced cascading questions:

Could we still move closer to our extended family? Could we afford career switches to meaningful work? What safety nets did we need to make this possible?

Here’s the financial foundation we built before making the leap:

CPF at Full Retirement Sum Created our first retirement safety net, especially critical when becoming self-employed

Staggered Career Transition We planned our transitions in stages so we wouldn’t lose all our income simultaneously, allowing us to manage monthly household expenses even with potentially reduced combined income

Income-Focused and Growth Portfolio Income portfolio structured to cover any shortfall in our monthly household expenses, including mortgage payments. When dividends weren’t needed for living expenses or there are surplus savings, they will be reinvested into our long term growth portfolio.

3 Years of Mortgage Payments in CPF OA Additional housing security that removed our biggest fixed expense from the worry equation

3 Years of Living Expenses in Cash and Bonds True emergency fund extending well beyond the conventional 6-12 months. Any unused portion could become dry powder if investment opportunities arose.

This allocation wasn’t about maximizing returns. It was about creating conditions where we could make decisions based on values rather than financial pressure.

It didn’t optimize for performance. But it gave us something more valuable: the peace of mind to make a leap that changed our lives.

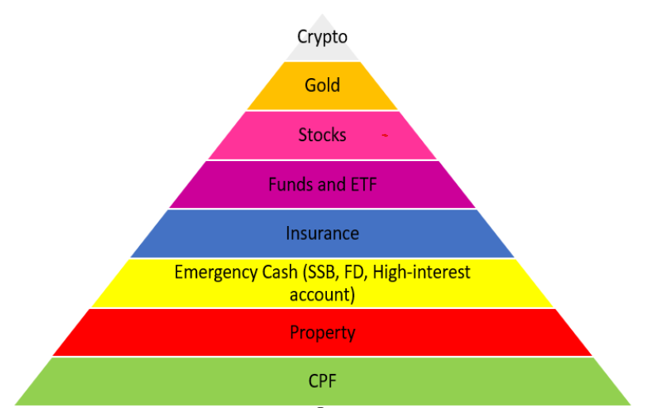

My Financial Foundation Framework: Financial Pyramid

I think about asset allocation in broad buckets, with each layer serving a distinct purpose.

Every financial pyramid will look different for everyone. This isn’t a template to copy, but a way of thinking—building from a strong, low-risk foundation to protect the downside and taking on higher risk gradually, with smaller allocations as we move upward.

The goal isn’t optimization. It’s resilience.

CPF — The Financial Safety Net

At the base sits CPF. For Singaporeans, it provides capital protection, guaranteed returns, and tax efficiency. It forms the core safety net—money that compounds steadily and anchors long-term security.

Its role isn’t excitement. It’s certainty.

Purpose: Long-term security, downside and creditors protection, and a stable retirement foundation.

Property — A Real Asset Foundation

Property adds tangibility to the portfolio as well as a roof over your head to reduce uncertainty. It serves as a long-term store of value, offers a degree of inflation protection, and grounds wealth in something real and functional. When managed prudently, it enhances stability without dominating the overall plan.

Purpose: Inflation hedging, diversification, and long-term asset backing.

Emergency Cash and Bonds — Liquidity and Optionality

Liquidity supports everything else.

This includes emergency reserves, opportunity funds, and operating buffers. While many aim for six to twelve months of expenses, we hold a larger buffer for flexibility and peace of mind.

Cash often feels unproductive in good times. But when conditions tighten, it becomes invaluable. Alongside cash, government and corporate bonds help preserve capital and cushion drawdowns, making volatility easier to live with.

Purpose: Capital preservation, emotional resilience, and the ability to respond calmly when conditions change.

Insurance — Risk Transfer

Insurance doesn’t grow wealth. It protects it.

It transfers the financial impact of illness, disability, or death—ensuring that one bad outcome doesn’t undo decades of careful work and investment gains. Insurance isn’t pessimism. It’s responsibility.

Purpose: Protection against irreversible financial loss and life disruption.

Funds, ETFs, and Stocks — Growth Assets

This layer drives long-term wealth creation.

The focus is global diversification — Developed markets, Asia, Emerging markets etc — supplemented by smaller tactical exposure to higher-growth areas. These assets protect purchasing power over time but come with volatility, which is why they sit higher in the pyramid.

Purpose: Long-term growth, wealth compounding, and inflation protection.

Physical Gold — Insurance, Not Growth

Gold plays a narrow but important role. It sits outside the financial system, doesn’t generate income but it provides protection during periods of crisis or loss of confidence.

Gold isn’t a return driver. It’s insurance.

Purpose: Portfolio insurance, regime-change protection, and behavioral stability.

Crypto — Digital Money and New Digital Gold

A small allocation to learn about the future of money and technology—something hedged outside the traditional fiat monetary system which has been around for many centuries. It warrants a small allocation so that we continue to learn as the world order evolves and regime changes.

Purpose: Portfolio insurance, regime-change protection, and behavioral stability.

The Principle

As you move up the pyramid:

- Risk increases

- Allocations starts small but potentially grow across time

- Strong foundations allows us to take on more risk

Not every dollar needs the same risk or volatility. Not every asset needs the same job.

A well-constructed pyramid allows the portfolio to fade into the background—quietly supporting life, work, family, and learning—without demanding constant attention.

Life Stage Evolution

20s-early 30s: Aggressive accumulation

40s with family: Preservation matters alongside growth to support life goals

50s+ ahead: Gradual shift toward more stability, retirement income streams, healthcare flexibility

The shift reflects changed priorities: sleep quality matters alongside returns, supporting family takes precedence over maximizing wealth.

This allocation made our career pivot possible. Without adequate stability and liquidity, we couldn’t have taken the risk.

The All-Weather Concept

Ray Dalio’s framework asks: what portfolio performs reasonably across different regimes?

- Rising growth: Equities perform well

- Falling growth: Bonds and cash provide stability

- Rising inflation: Real assets protect value

- Falling inflation: Bonds and cash appreciate

No single asset does well everywhere. But a thoughtful combination weathers all adequately.

We didn’t know how long establishing new income would take, which environment we’d face, or what challenges would arise. So we built for multiple possibilities rather than betting on one outcome.

Portfolio Resilience: Two Capabilities

True resilience requires:

Staying power – Ability to stay invested through volatility without panic selling

Opportunity – Ability to deploy capital during downturns

Both matter equally. Our allocation maintained both during transition: enough stability to stay calm, enough liquidity for opportunistic moves.

Financial Independence as Infrastructure

FI should complement your life, not become it.

The portfolio exists to support meaningful work, family time, personal growth, health, relationships, experiences. If managing it requires constant attention or generates persistent anxiety, something is misaligned.

My framework aims for sustainability: a portfolio that compounds for decades while requiring minimal intervention, working quietly in the background.

Our career transitions were possible because the portfolio was designed to enable life choices, not restrict them. It gave us optionality to pursue purpose over paychecks.

That’s the true measure of portfolio resilience: Does it enable the life you want, or demand a life you don’t?

The Real-World Test

The scenario planning from our Great Resignation shows this in practice. We ran multiple scenarios, stress-tested outcomes, built buffers for unexpected challenges.

The allocation we’d built over 15+ years passed the test—not perfectly, but adequately. We could afford the pivot, move homes, weather income disruption, wait for right opportunities rather than desperate ones.

None guaranteed. But possible because allocation created infrastructure, not just returns.

Next in Part 3 Lessons from the 1929 crash about cash reserves and opportunity, drawing on Benjamin Roth’s firsthand account of the Great Depression.

This is a personal reflection on how I think about investing over time. It’s shaped by my own circumstances and priorities, and isn’t intended as financial advice. Everyone’s situation is unique, and what works for me may not work for you. Consider consulting with a qualified financial advisor for personalized guidance.