Two books sat on my reading list for very different reasons. Both ended up teaching me the same lesson.

The Great Depression: A Diary by Benjamin Roth is a quiet, intimate account—a lawyer in Youngstown, Ohio, documenting his observations and financial decisions from 1929 through the 1940s. His diary entries are remarkable for their immediacy and honesty.

1929: Inside the Greatest Crash in Wall Street History by Andrew Ross Sorkin is the opposite in style—sweeping, cinematic, and meticulously researched. The #1 New York Times bestseller brings to life the greed, euphoria, and human folly that led to an era-defining collapse, told through the larger-than-life characters who drove the boom and then watched it all unravel.

Together, they offer something no single account could: both the bird’s-eye view of the crash and the ground-level human cost of it.

What struck me most from both wasn’t the scale of collapse—stocks fell 89% peak to trough, unemployment hit 25%, banks failed by the thousands.

It was something far simpler: those who had cash could buy extraordinary assets at historic discounts, while most people had no cash at all.

The biggest opportunity of the century arrived precisely when almost no one could capitalize on it.

The Irony of the Great Depression

Roth writes extensively about opportunities he witnessed but couldn’t fully exploit—quality stocks at 10-20% of former values, prime real estate for fractions of replacement cost, businesses for pennies on the dollar.

The problem: he had limited cash and no income security. Most entries express frustration watching opportunities pass while scrambling for basic living expenses.

Sorkin’s account adds the other dimension—showing how the very architects of the boom, financiers who had seemed invincible, were equally exposed when the tide turned. Leveraged to the hilt, many lost everything overnight. Even those at the top of the system couldn’t protect themselves when confidence collapsed.

Meanwhile, those who entered the Depression with cash—mostly wealthy families and a few foresighted individuals—could accumulate assets that would compound for generations.

John D. Rockefeller said during the crash: “These are days when many are discouraged. Prosperity has always returned and will again.”

Easy to say when you have resources. Roth knew recovery would come eventually—but couldn’t participate because survival took precedence over investment.

The lesson from both books is identical: opportunity requires capacity—and capacity comes from preparation before the crisis, not during it.

Why Most People Had No Cash

The 1929 crash followed years of speculation, margin buying, and euphoric optimism about perpetual prosperity.

Sorkin captures this vividly—a nation swept up in the intoxicating belief that markets only moved in one direction. Sound familiar?

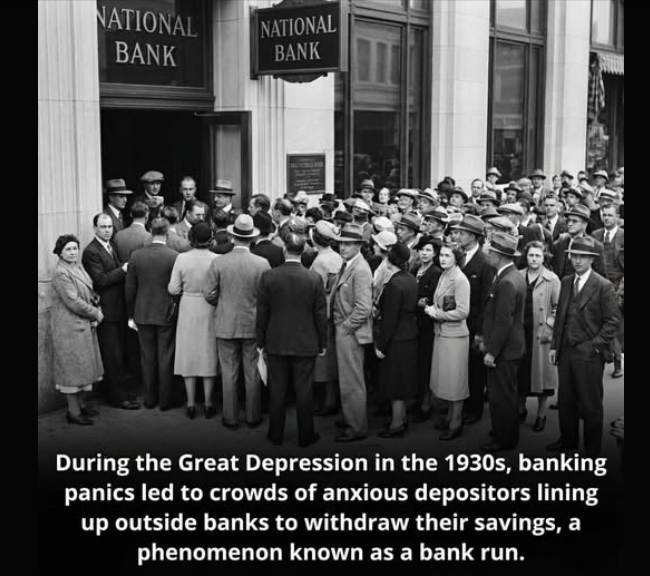

People were fully invested—not just in stocks, but leveraged through margin loans. When markets fell, margin calls forced selling at terrible prices. Banks failed, wiping out deposits. Jobs disappeared, eliminating income. Credit dried up completely.

Those without cash reserves faced impossible choices: sell assets at depression prices to survive, or hold and risk losing everything.

Meanwhile, the wealthy and cautious—those who maintained cash despite opportunity cost during the boom years—could buy quality assets from desperate sellers at generational prices.

As Roth documents repeatedly: “The man with cash is king.”

But very few had cash when it mattered most.

The Opportunity Cost Debate

This raises the question I wrestle with constantly: how much cash is enough?

Cash earns essentially nothing. During bull markets, it actively hurts performance. In 2023-2024, holding 15% cash meant missing significant equity gains. That stings when you watch your portfolio lag benchmarks.

But both books suggest opportunity cost is entirely the wrong framework.

Cash isn’t about maximizing returns during normal times. It’s about maintaining optionality during abnormal times—and abnormal times arrive without warning.

Better question: What’s the cost of NOT having cash when you desperately need it?

For Roth and millions like him, the cost was missing generational wealth-building opportunities. For the financiers in Sorkin’s account, the cost was complete ruin. For ordinary families, it was worse—losing homes, businesses, and livelihoods.

That reframes cash not as a drag on returns, but as portfolio insurance and opportunity enablement.

How This Shapes My Approach

I maintain two distinct cash reserves serving very different purposes:

Emergency Fund (Defensive) At least twelve months of family expenses in highly liquid accounts. Pure insurance for job loss, health crises, or unexpected expenses. This is sacred—never deployed for investments, no matter how attractive the opportunity appears.

Purpose: psychological stability and lifestyle protection, not returns.

Opportunity Fund (Offensive) Additional cash—typically ranges between 10-20% of investable assets—waiting specifically for market dislocations. Deployed during corrections and crises: March 2020, portions during 2022 volatility, whenever fear spikes and quality assets go on sale.

This earns nothing most of the time. That’s fine. Its value comes entirely from being there when needed.

Warren Buffett’s Cash Pile

Berkshire Hathaway currently holds approximately $381 billion in cash—roughly 32% of total assets.

Critics call this wasteful. But Buffett isn’t stupid or scared. He’s patient and prepared.

He maintains this position because it provides flexibility to act decisively when opportunities appear, stability during stress with no forced selling, and independence from external capital markets.

Most importantly, it allows being greedy when others are fearful—the exact advantage Roth witnessed the wealthy exploit during the 1930s and Sorkin’s research confirms was the decisive edge.

I apply the same principle at my own scale.

The Discipline of Not Deploying Too Early

Maintaining cash discipline during bull markets requires resisting constant temptation.

Markets rise for months or years. Your cash lags. Friends share portfolio gains. Every headline touts new highs. The psychological pressure to deploy becomes intense—you feel foolish holding cash while missing “obvious” opportunities.

This is precisely when discipline matters most.

Sorkin’s account makes this vivid: the 1920s boom lasted years, drawing in ordinary people who had never invested before, convinced they were missing out. Those who stayed fully invested until 1929 lost everything. Those who held cash—even at significant opportunity cost—could capitalize on the crash.

But they had to resist deploying too early. Real opportunities came when sentiment collapsed completely in 1930, 1931, 1932—long after most had exhausted their resources and hope.

I don’t pretend to time this perfectly. But if I’m always fully invested, I’ll never have capacity when it truly matters.

2020: A Modern Example

March 2020 provided a condensed version of this dynamic. COVID triggered the fastest crash in history. Quality stocks fell 30-40% in weeks. Fear was absolute.

Those with cash bought at March lows and captured extraordinary recoveries. Those fully invested—or worse, leveraged—could only watch helplessly or panic-sell at the bottom.

I had meaningful cash positions. Not because I predicted a pandemic—nobody did—but because I maintain cash as standard practice. That allowed me to deploy during March and April when others couldn’t. Not heroically or perfectly, but calmly and deliberately.

The experience reinforced the lesson from both books: opportunity arrives suddenly, and capacity must exist beforehand.

Cash as Freedom

Ultimately, cash reserves provide something more valuable than returns: freedom.

Freedom from fear during volatility. Freedom to make decisions based on opportunity rather than necessity. Freedom to wait for genuinely attractive entry points rather than chasing momentum.

This connects back to the core principle of this series: financial independence should complement your life, not dominate it.

Both Roth’s diary and Sorkin’s panoramic account confirm that the crash didn’t just destroy wealth—it destroyed options. Those without cash lost the ability to choose. Those with cash kept it.

That peace of mind is worth far more than the opportunity cost of holding “unproductive” cash.

In Part 4, I’ll share why I added physical gold to my portfolio in 2024—a decision that surprised even me but fit naturally into this resilience framework.

This is a personal reflection on how I think about investing over time. It’s shaped by my own circumstances and priorities, and isn’t intended as financial advice. Everyone’s situation is unique, and what works for me may not work for you. Consider consulting with a qualified financial advisor for personalized guidance.