With so much debate about the sandwich class recently, I tend to think that perhaps this is the generation with the highest proportion of this population thus far. We are often confronted with multiple challenges that stretches us financially, including not just supporting ourselves, but our children and even aging parents, while at the same time, planning for our own retirement. Parents’ allowance is something probably pretty unheard of in countries like the US or in Europe. The US financial bloggers seldom talk about parents allowances and their FIRE plans are usually centered around just having enough money to support their own family.

In Singapore, our grandparents were mostly immigrants. So they started out really poor, and had less income generating power. The first generation spent most of their resources raising the second generation. It trickles down like a domino effect but the responsibility towards giving parent allowance might slowly dissipate with wealth accumulation as our economy continues to grow. For us, we do not really expect our offspring to support us during retirement as we have our own retirement plans. In fact, even our parents have some form our retirement planning in place although not substantial. But living standards has definitely improved a lot as compared to our grandparents generation.

Look at how much Singapore has progressed in less than 20 years

Last year, there were changes to our finances, especially the fact that Kate was away on sabbatical meant that we were living off one income for the most part. Also, with the addition of Ashton, it also meant an additional mouth to feed.

The stock market was also rather unpredictable more often than not, which also affected our net worth collectively.

At our current financial status, we are not afraid to lose our job should there be any form of retrenchment or stock market going into bear territory. We are also exploring the possibility of another sabbatical should the opportunity arise.

Granted that we have not attain financial independence, the peace of mind that comes with financial stability is absolutely priceless. Here comes the numbers!

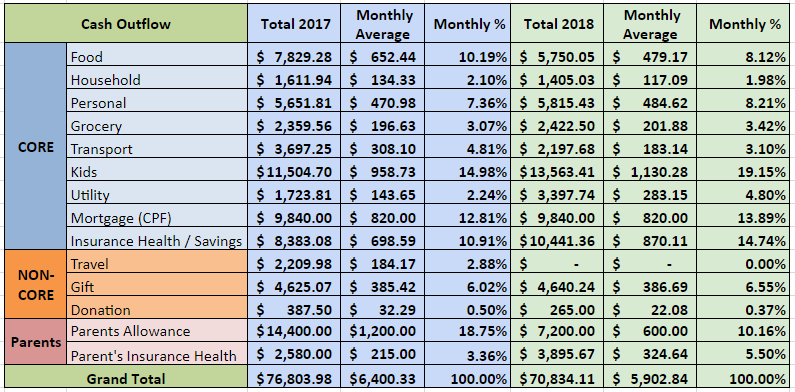

Our 2018 expenses

You may refer to our 2017 – Cash outflow analysis

The biggest chunk of our cash outflow was previously parents allowance ($14,400 – 18.75%) but has since decreased to ($7,200 – 10.16%) ever since we top up our parents CPF upfront in July 2018 and now they are enjoying monthly payouts via CPF Life.

For 2018, our top 3 cash outflows are:

1. Kids – $13,563.41 (19.15%)

For the kids category, there is an increase of approximately $2k after the inclusion of Ashton into our family last year. We anticipate that this would trend upwards when they are still in childcare and likely to taper off slightly after they enter primary school which includes their enrichment classes.

2.Insurance – Health ($2,973.26) and Savings ($7,468.10) – $10,441.36 (14.74%)

For the insurance category, about $7,468.10 are put towards savings insurance plans for our family and $2,973.26 for our health insurance. Most people do not treat savings insurance plans as part of their expenses. But we included insurance savings as part of our cash outflow with the reason that we will most probably still be paying for some of them even though we might have reached FI. We do acknowledge that this is not an expense but it is still a cash outflow nonetheless unless we monetize the accrued cash value of the savings policies. Some of our savings plan will be fully paid up within the next 5 years which will bring this figure down but will be partially offset by the increasing health insurance for our family of four.

3.Mortgage – $9,840 (13.89%)

For the mortgage category, we are paying using our CPF. Its a 20 year bank loan (First 3 years fixed interest and floating on the 4th year onward pegged against the FHR9 rate). We would like to maintain an arbitrage on this home loan as the interest is currently less than 2%. We are currently in the midst of setting aside enough CPF / cash to pay off this mortgage should the interest rate spike up when we reach FI. So we should not be seeing this in our cash outflow when we reach FI once we set aside enough funds.

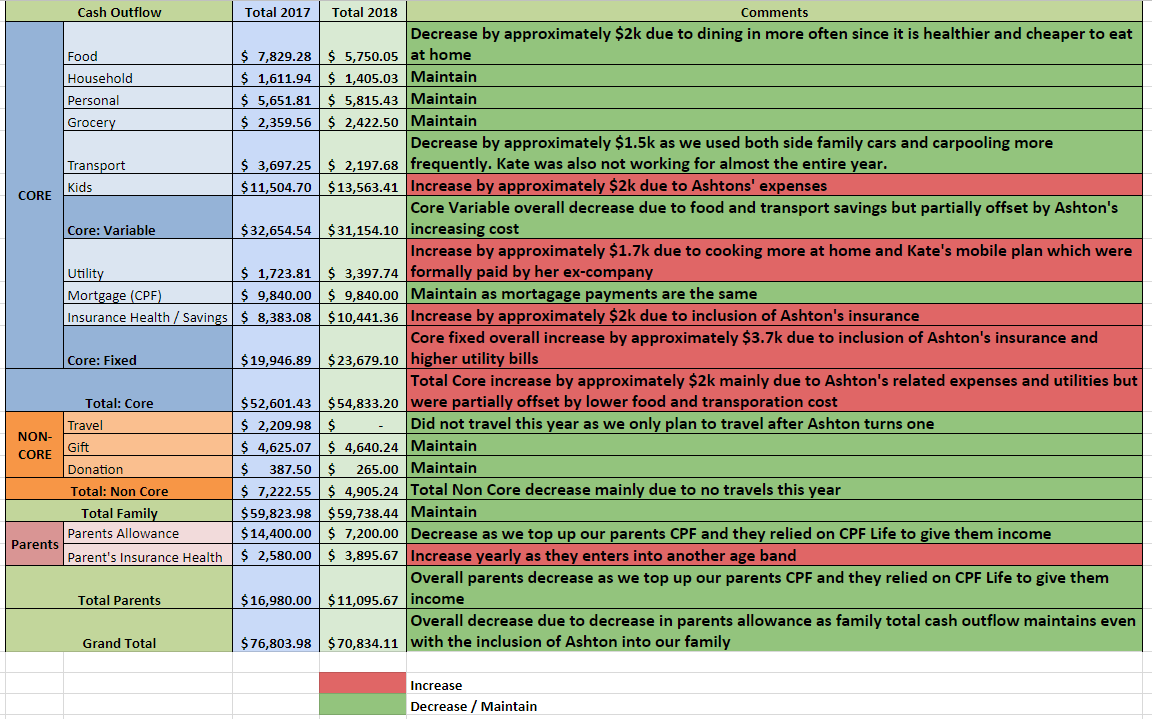

Summary for 2018

Family ($59,738.44)

Our total family cash outflow is almost the same as last year even with the inclusion of Ashton in our family. The increase of Ashton’s cash outflow were partially offset by lower transport cost, lower food costs and no travels in 2018. Lower transport cost are due to our parents ferrying us around more often and Kate for not working for almost the entire year of 2018. Lower food costs were also attributed to cooking more at home and dining less at restaurants. This doesn’t mean we compromise on our quality of the food as we eat healthier food at home. Thankfully, our parents cook for us frequently as we are busier with two kids in our household nowadays. Travelling took a step back this year. However, we do not feel like we are missing out much without travelling as we enjoyed more time with our two kids. As Kate mentioned previously – you do not need to travel to feel happy.

It comes from finding inner peace, understanding yourself, seeking awareness of where you are at each point in life, and also most importantly, the time and energy to contemplate about them.

Parents ($11,095.67)

This was greatly reduced as we topped up our parents CPF which will allow them to draw a monthly allowance from CPF Life which works like an annuity. So basically we front-loaded our parents allowances so that we do not have to pay them cash anymore as they will be relying on their CPF Life. But we will still be paying for their health insurance which should slowly increase year after year.

Overall ($70,834.11)

Overall total cash outflow decrease by almost $6k due to lesser parents allowances and going forward, this category should be minimal. So with the parents allowance and mortgage gone when we reach FI, our total cash outflow should be in the range of $54k per year / $4.5k per month. We did not travel this year as we feel that Ashton is still too young, we will need to ramp up this category by another $6k for travels in 2019 to round off our budget total cash outflow at $60k per year / $5k per month (exclude mortgage of approximately $10k) for 2019 which coincides with our target FI cash outflow.

We hope that this will provide a reference of how a household expenditure pattern for a family with two kids living in Singapore. We do not intent for this to be some sort of competition or comparison but we are trying to showcase our minimalist lifestyle by not spending more to enhance our happiness. We are also not scrimping and saving to the core. We are seeking to strike a nice balance between spending, saving and happiness.

What about you? What are your money goals for 2019?

Do stay tune and hope you have a great year ahead!

So you guys have close to $2m in stocks and bonds?

Nope